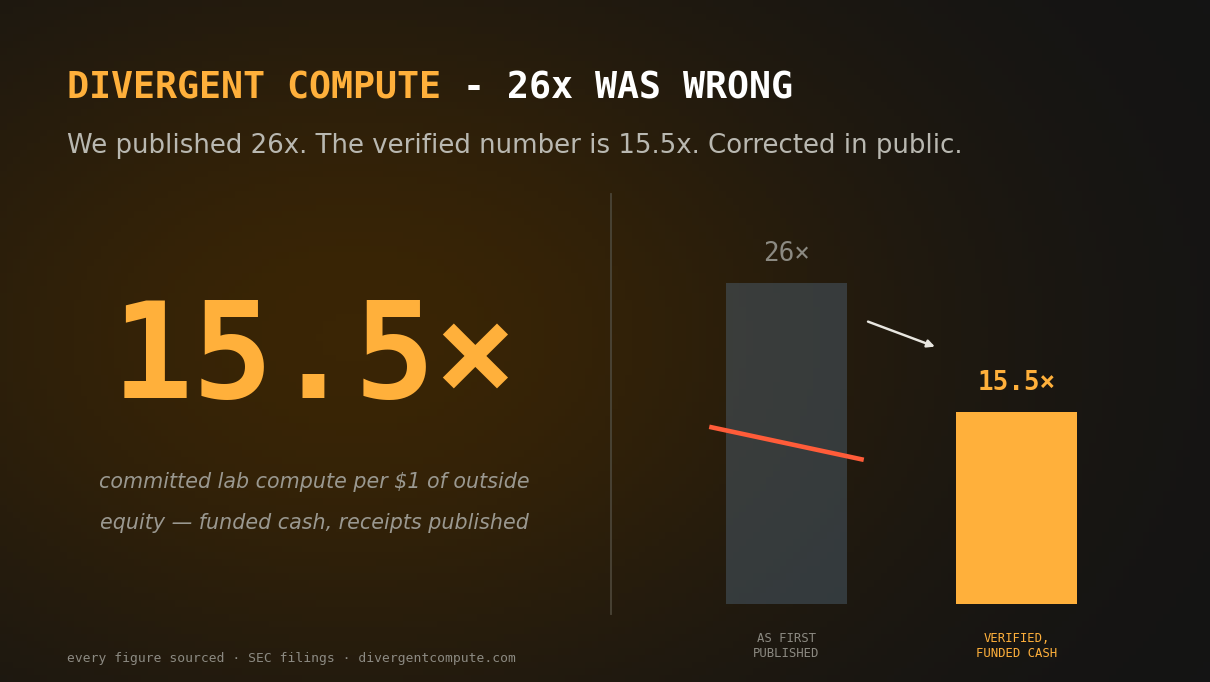

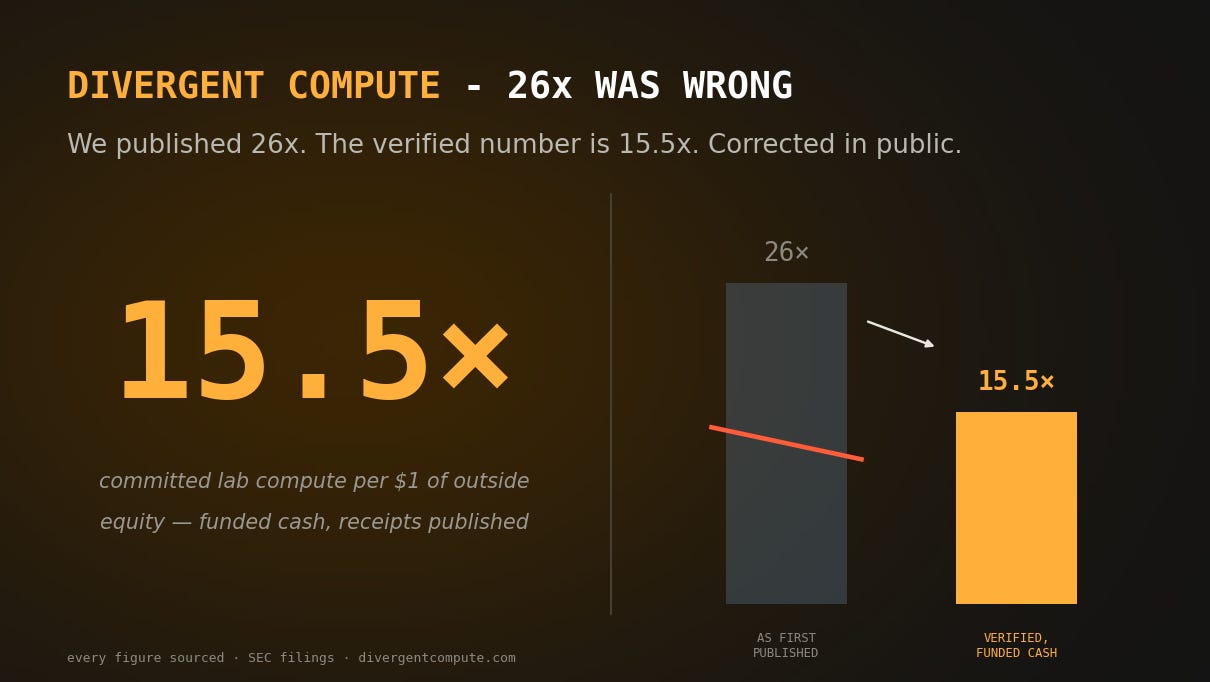

26x was wrong. The real number is 15.5x — and the loop got tighter.

We re-verified every figure against the SEC filings themselves. Eight confirmed, three corrected — including our own headline.

On July 2 we re-verified every headline figure we have ever published against the text of the SEC filings they came from. Not the press coverage of the filings. Not the databases built on the filings. The filing text itself, accession by accession.

Eight figures confirmed verbatim. Three required correction. One of those corrections cut our own headline number by 40 percent — and this article is the story of why we published that correction within hours, on every surface we operate, and why we think the corrected picture is more concerning than the one it replaced, not less.

What we had published

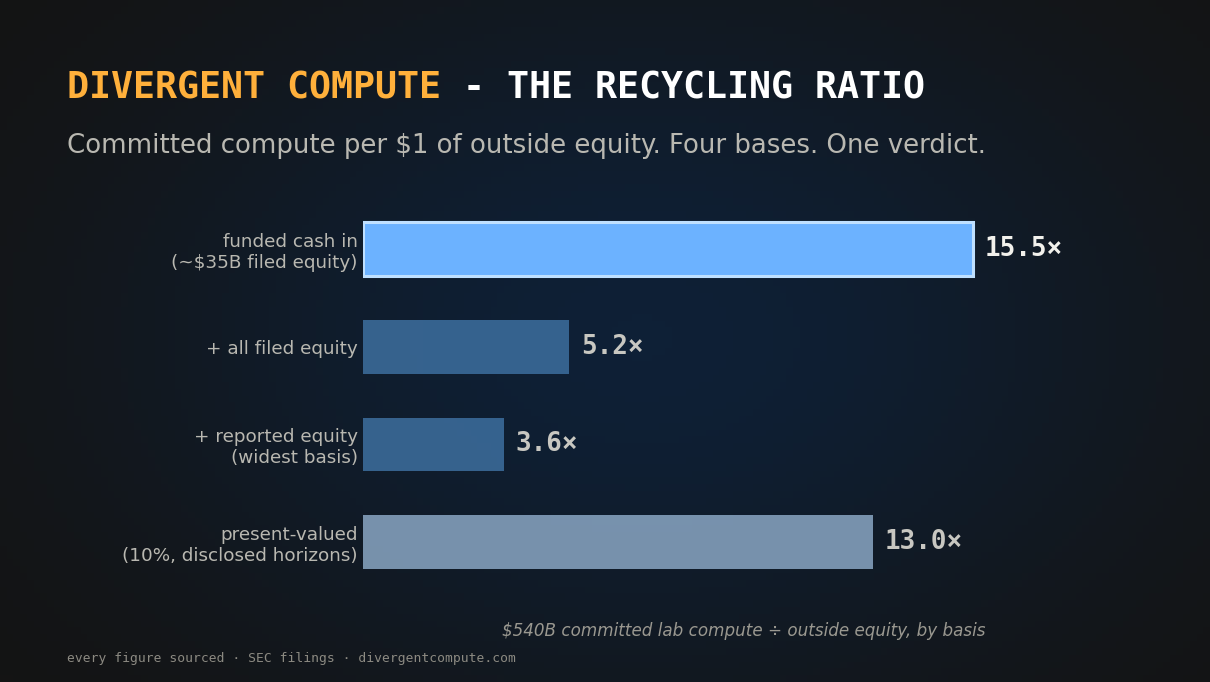

The recycling ratio is our central measurement of the AI build-out’s circular financing. The idea is simple: take the compute the leading AI labs have contractually committed to buy from the hyperscalers — roughly $540 billion across OpenAI, Anthropic, and xAI — and divide it by the outside equity actually funded into those labs. The ratio tells you how much demand rests on each dollar of real outside capital.

Through July 1, we published that ratio as approximately 26x: $540 billion of committed compute resting on roughly $21 billion of filed, funded equity.

What the filing said

Amazon’s Q1 2026 Form 10-Q, accession 0001018724-26-000014, contains this sentence:

In Q1 2026, we invested $15.0 billion in Series C Preferred Stock of OpenAI… and entered into a commitment letter to invest an additional $35.0 billion.

Our edge ledger — the EDGAR-verified graph of every disclosed investment, compute commitment, supply relationship, and mark-to-model gain across the AI compute complex — did not contain that edge. We had Amazon’s $8 billion into Anthropic. We had Microsoft’s $13 billion into OpenAI. We missed Amazon’s $15 billion into OpenAI.

Adding the funded $15 billion widens the outside-equity base from roughly $21 billion to roughly $35 billion. The recycling ratio compresses from 26x to 15.5x. Present-valued at 10 percent over each commitment’s disclosed horizon, it reads about 13x.

We updated the ledger, re-ran the toolkit, re-rendered both published papers, corrected every page of the site that carried the number, and logged the correction — dated, with the accession — on our public receipts ledger. Same day.

Why the corrected picture is tighter, not looser

Here is what the correction does not mean: it does not mean the loop loosened.

Our falsifier ledger — the list of observations that would prove our thesis wrong, published in advance — includes this one: the ratio falls as outside equity grows. If genuinely arm’s-length capital enters the labs faster than new intra-ring commitments, the funded-cash ratio compresses toward an ordinary supplier-financing level.

The ratio fell. So did the falsifier trigger?

No — and the reason is the whole story. The new equity is not arm’s-length capital. It is the second-largest cloud provider taking a $15 billion stake in the largest lab committed to its own datacenters — the same lab that has committed $138 billion of compute purchases to that same provider’s cloud. Amazon now sits on both sides of its own largest customer relationship, exactly as Microsoft does with its OpenAI stake and Azure commitment.

Both of the top two clouds now hold equity in the lab whose compute commitments underwrite their capital expenditure. The multiple fell because the circle got tighter. A dollar of outside equity that comes from inside the ring is not outside at all — which is why we report the ratio on multiple bases and let the structure, not a single number, carry the argument.

The mechanism, in one walk

Follow one dollar around the loop. A hyperscaler invests in an AI lab. The lab commits that capital — and much more — to buy compute from the hyperscaler’s cloud. The hyperscaler books the commitment and builds datacenters against it, buying chips with the capex. And when the lab’s valuation rises, the hyperscaler books a paper gain on the stake — Microsoft recorded $5.9 billion of net gains on its OpenAI position in the nine months through March 2026, primarily a dilution gain from OpenAI’s recapitalization; Amazon recorded a $12.3 billion upward adjustment on Anthropic in a single quarter.

Capital out. The investor’s own revenue back. A paper profit on top. Every leg in a filed document.

The 2000 telecom cycle ran the same pattern with different instruments — vendors lending carriers the money to buy their equipment, booking the loans as revenue. Lucent extended roughly $15 billion of vendor financing against roughly $300 million of operating cash flow. When the demand the loans had manufactured failed to materialize, the receivables became losses, and the sector lost more than $2 trillion of market value.

We are not predicting a repeat. We are measuring a structure. The structure rhymes.

Why we correct in public

A research desk that only publishes numbers moving in its thesis’s favor is running marketing, not measurement. Ours works the other way: the ledger is open data, the toolkit that computes the ratio is open source, the falsifiers are stated before the calls, and when we find our own error, the correction ships the same day with the receipt attached.

Twenty-six was wrong. Fifteen and a half is what the filings support today. When the next filing changes it — in either direction — you will read it here first, with the accession.

The live ledger, the falsifier watch, and the correction trail: The Ground Truth Tape · Receipts · Falsifier Watch