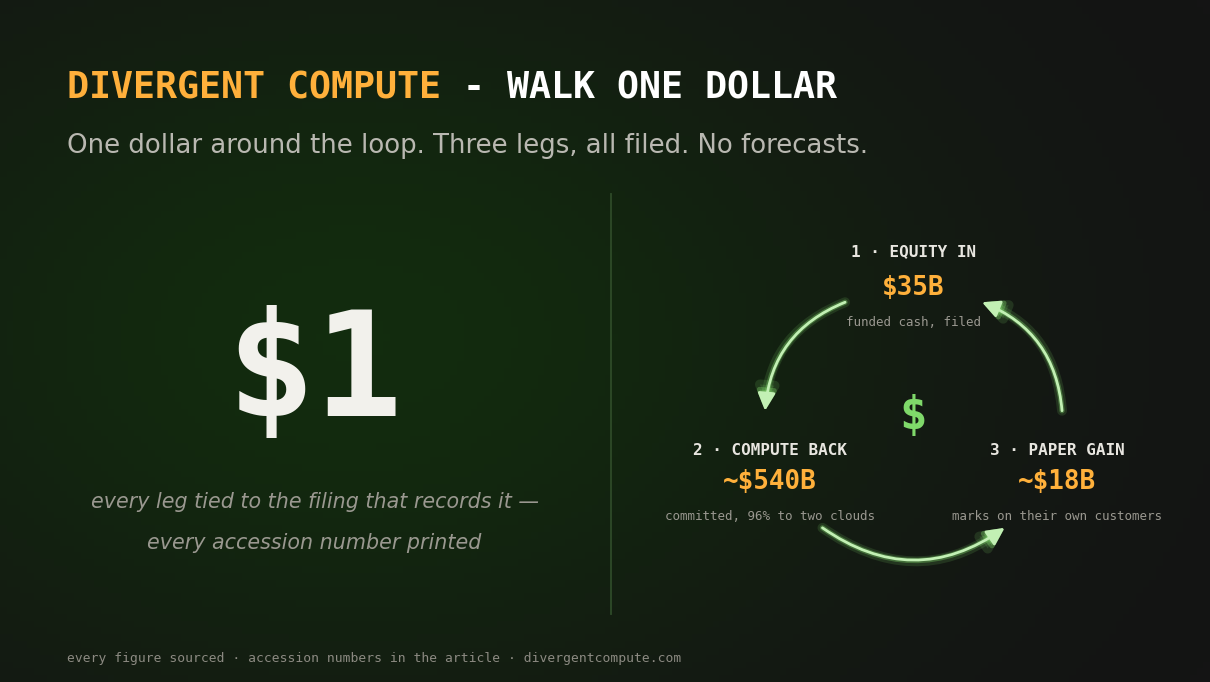

Walk One Dollar

No forecast, no opinion about the future. One dollar around a loop that already exists, each leg tied to the filing that records it.

Most arguments about the AI build-out are arguments about the future: demand curves, model capabilities, adoption rates. Reasonable people disagree about the future indefinitely. This article makes no claim about the future at all. It walks one dollar around a loop that already exists, leg by leg, and names the filed document that records each leg.

You do not have to take our word for a single step. Every accession number is printed. The walk takes five minutes; the filings are public; the loop is real.

Leg one: the equity goes in

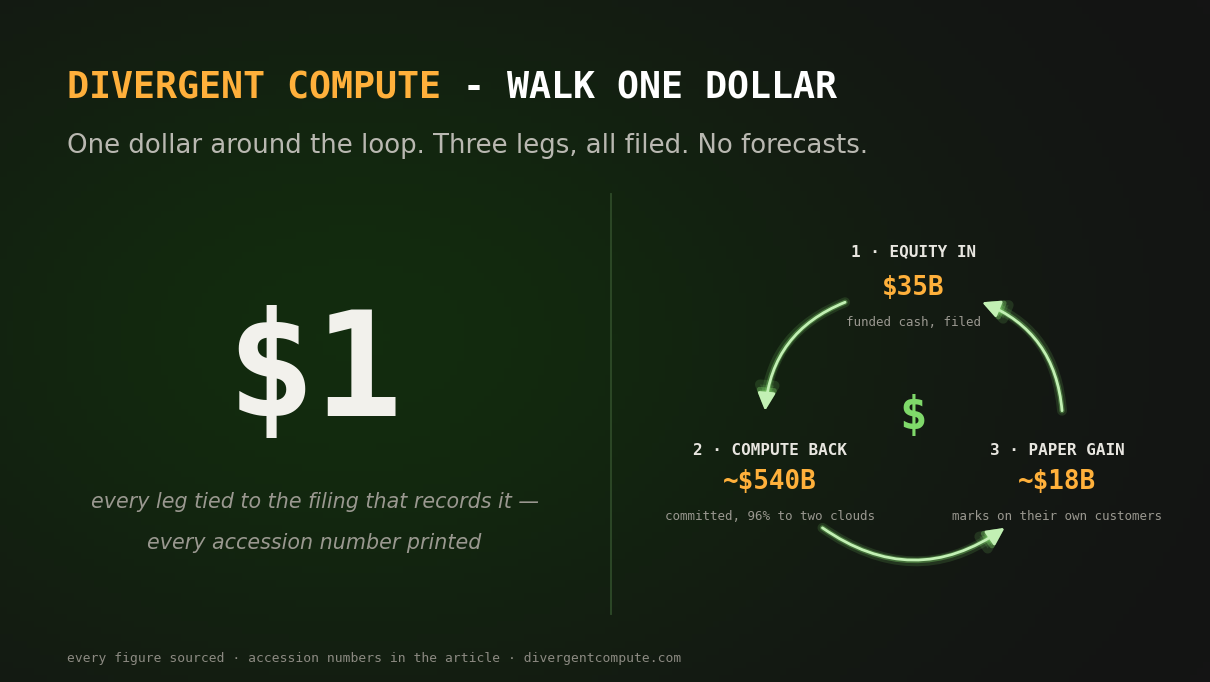

In October 2025, Microsoft’s restructured OpenAI position carried total funding commitments of $13 billion — $11.8 billion funded as of March 2026. In the first quarter of 2026, Amazon invested $15.0 billion in OpenAI’s Series C preferred stock and signed a commitment letter for an additional $35.0 billion. Amazon also holds $8 billion of Anthropic, converted to preferred stock.

Sources: Microsoft 10-Q accessions 0001193125-25-256321 and 0001193125-26-191507; Amazon 10-Q accession 0001018724-26-000014. Filed dollar amounts, not press figures.

Leg two: the compute comes back

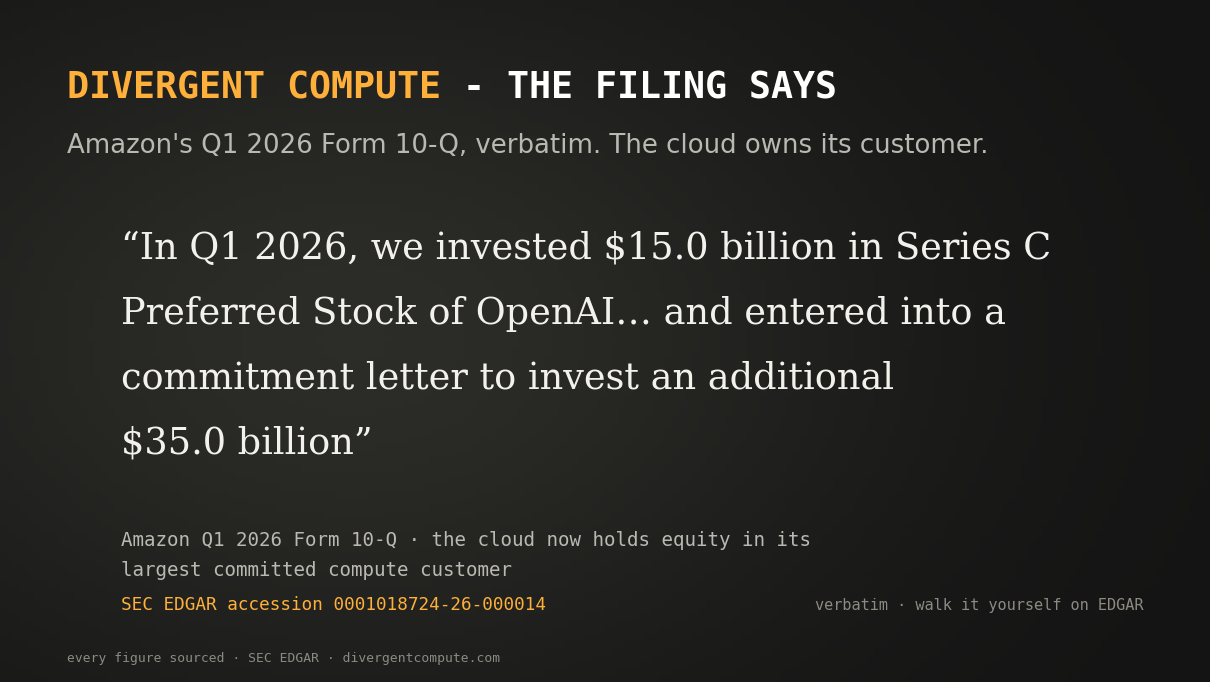

The same filings record what the labs committed in return. OpenAI: an incremental $250 billion of Azure services — Microsoft’s own 10-Q language — and $138 billion of compute committed to AWS, disclosed as an existing $38 billion commitment expanded by $100 billion over eight years. Anthropic: $100 billion to AWS over ten years, $30 billion to Microsoft’s cloud.

Add the smaller filed legs and roughly $540 billion of committed lab compute routes through the complex — 96 percent of it to just two providers, the same two firms that are among the labs’ largest equity holders.

The dollar that left as an investment comes back as the investor’s own cloud revenue. Or more precisely: as backlog — commitments booked years ahead of the cash, against labs whose own funding depends on the next financing round closing.

Leg three: the paper profit on top

There is a third leg most walks miss. When the lab’s valuation rises, the investor books a gain on the stake — earnings recognized on the appreciation of one’s own customer.

Microsoft recorded $5.9 billion of net gains on its OpenAI position in the nine months through March 2026, primarily a dilution gain from OpenAI’s recapitalization. Amazon recorded a $12.3 billion upward adjustment on its Anthropic preferred stock in a single quarter. Together: roughly $18.2 billion of paper gains, booked by the two firms that supply the compute those same labs are committed to buying.

What the walk establishes

Divide the committed compute by the outside equity actually funded into the labs and you get the recycling ratio: about 15.5 times on funded cash, about 13 times present-valued. We report it on every basis, because the honest range is the point — no basis lands it near an arm’s-length level.

The walk does not establish fraud, and we do not allege any. Every leg is disclosed; firms are entitled to invest in their customers. What the walk establishes is structure: a few balance sheets sitting on both sides of the same demand, commitments underwriting capex, and paper gains booked against the loop’s own appreciation. Structures like that are not wrong — they are fragile. The same dollar that validates the demand on the way out validates the earnings on the way back, and if one keystone steps away, every leg reprices at once.

The last industry that financed its own demand this way had four years of record earnings before the receivables turned. We measure this one in public, quarterly, with the accessions attached.

The full ledger, every edge, every filing: The Ground Truth Tape · the open data: Open Data