Dark Fiber, Again

A hyperscaler just announced it will sell its excess AI compute, and the stock rose 9 percent. The last cycle had a name for this.

This week a hyperscaler announced it will sell its excess AI compute, and its stock rose nine percent. The 2000 cycle had a name for this. It is worth remembering where the name came from, because the industry that coined it did not survive the lesson.

What dark fiber was

Between 1996 and 2001, American carriers invested more than $500 billion — most of it borrowed — into fiber, switches, and wireless. The investment thesis was a demand forecast: internet traffic doubling every hundred days, forever. Capacity was built years ahead of any contracted buyer, because the forecast said the buyers were coming.

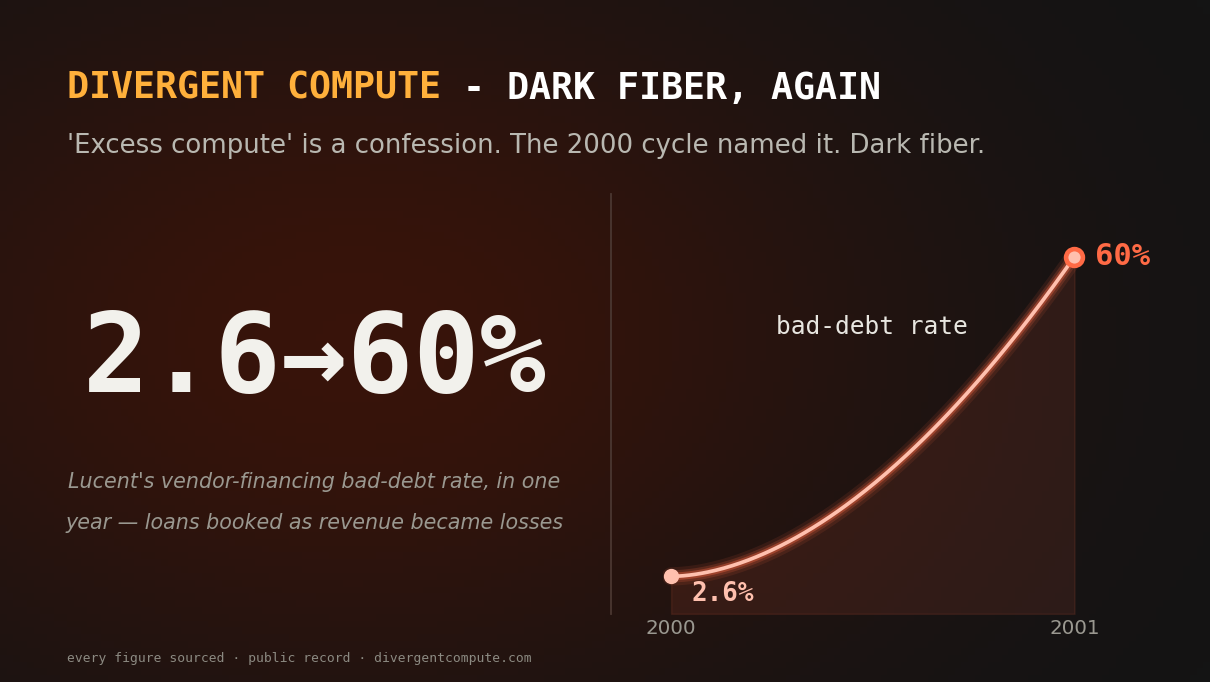

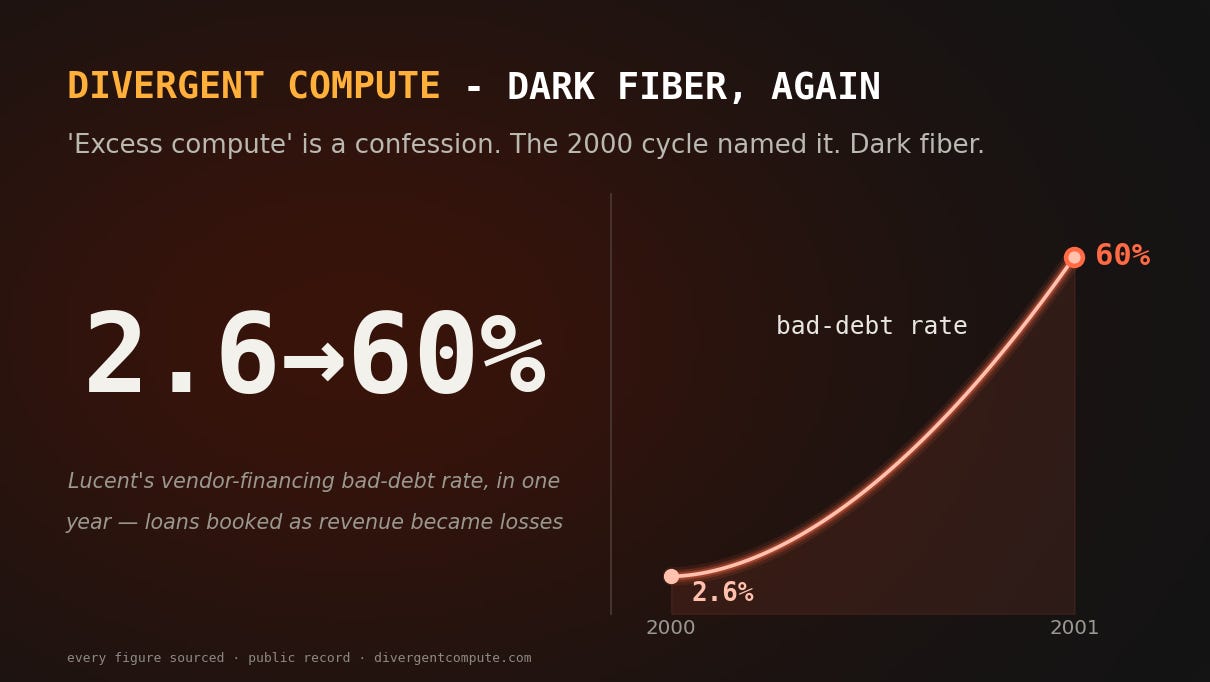

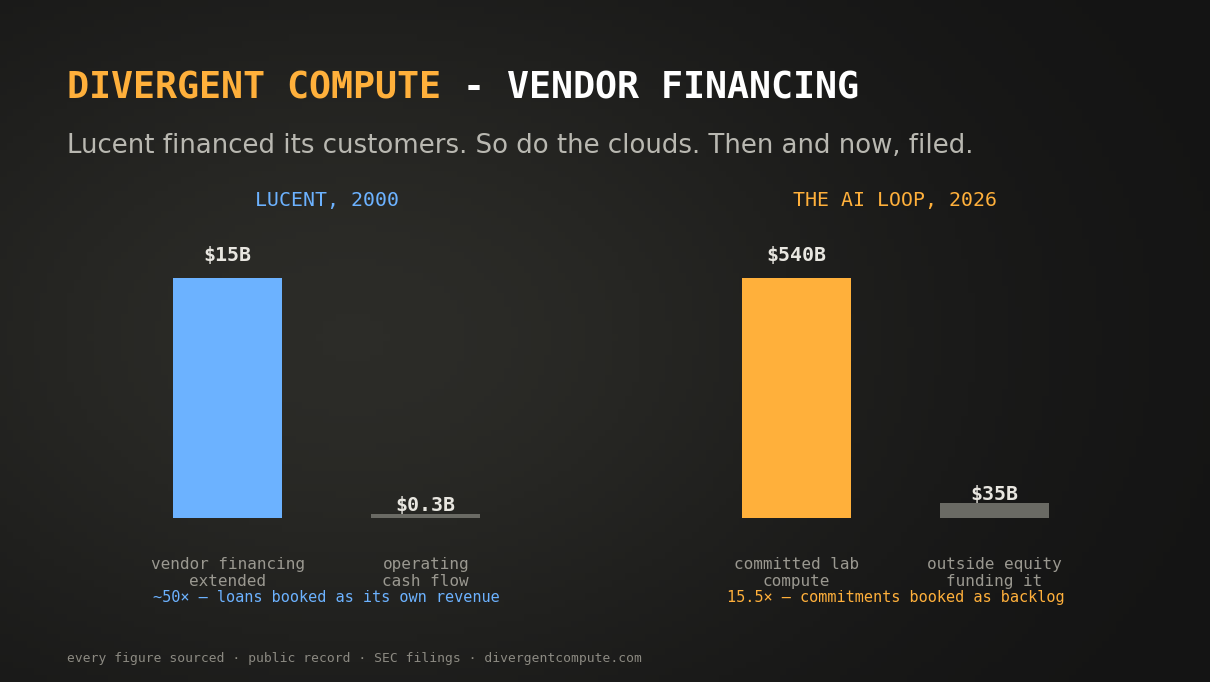

They were not coming — not at that rate. The fiber that cost billions sat unlit. The industry called it dark fiber: capacity so far ahead of demand that it had never carried a signal. By 2001, carriers were renting capacity to each other at any price, then to anyone, then going broke. The companies that had financed their customers’ purchases — Lucent extended roughly $15 billion in vendor financing against roughly $300 million of operating cash flow — watched loans they had booked as revenue become losses. Lucent’s bad-debt rate went from 2.6 percent to 60 percent in a year. Global telecom equities lost more than $2 trillion.

The tell, in hindsight, was not the crash. It was the moment capacity started hunting demand instead of the other way around.

The 2026 rhyme

“Excess AI compute” is the confession in two words. You do not build a cloud business to offload capacity you already have buyers for. The demand was supposed to be the point.

We logged this pivot on our public receipts ledger the day the news broke — not because one announcement proves a thesis, but because it is precisely the observable our published framework said to watch for. Our telecom chapter, written months earlier, ends with this sentence: the direct descendant of dark fiber is a hyperscaler announcing that it will rent out its excess AI compute.

The deeper structure matters more than the headline. In 2000, the vendors financed the demand for their own equipment. In 2026, the financing runs through equity instead of loans: the top two cloud providers now both hold equity stakes in the largest AI lab committed to their own datacenters. Roughly $540 billion of committed lab compute rests on roughly $35 billion of funded outside equity — about 15.5 times — and 96 percent of those commitments route back to just two firms. Different instruments. Same disease: demand that the suppliers themselves are financing, capacity built against commitments rather than cash, and paper gains booked on the appreciation of one’s own customers.

What would prove this wrong

We publish falsifiers in advance, so here they are. The dark-fiber read weakens if committed compute is drawn down and paid for out of external customer revenue rather than the next financing round. It weakens if genuinely arm’s-length capital enters the labs faster than intra-ring commitments grow. It weakens if the commitments spread beyond the two-cloud ring to a competitive set of buyers. And it weakens if the multi-year backlogs convert to cash on their disclosed schedules without renegotiation.

Any of those would be visible in filings within two quarters. We will report them the day they appear — that is what the receipts ledger is for.

Until then: the last time capacity started hunting demand, it had a name, and everyone learned it too late. This time the meter is running in public.

The live measurement: The Ground Truth Tape · the 2000 overlay: AI vs Dotcom · every correction we’ve made: Receipts