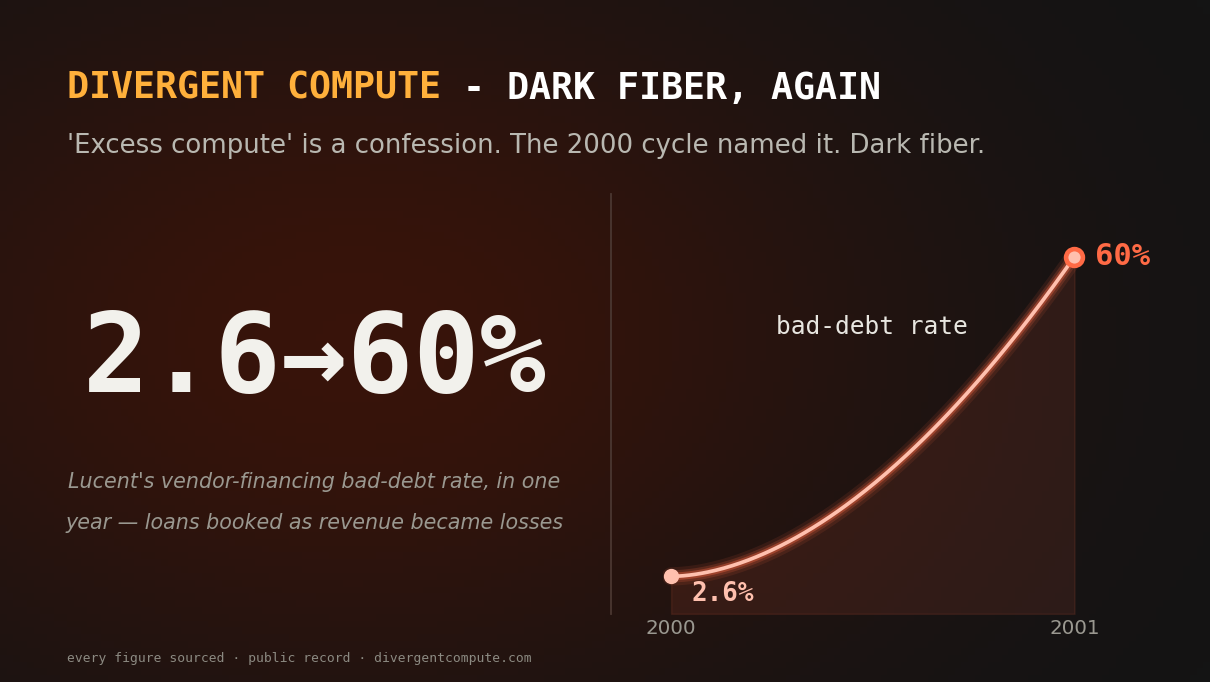

Real demand, or the same dollar taking a second lap?

Headline AI revenue is growing fast. The question that decides whether it's a business or a bubble is who's paying — and in the clearest case, the answer is the people who funded it.

Revenue growth alone clears the headline band for most of the AI complex — CoreWeave at 168%, Broadcom at 64%, four more firms clustered at 32–36%. Impressive numbers. But the question that actually matters is not the rate of the growth; it is the source.

The anchor is uncomfortable. MIT's NANDA study found that roughly 95% of enterprise GenAI pilots show no measurable P&L impact (Fortune, August 2025). So in our framework, fast revenue growth scores well only when it is paired with demonstrated paid retention and pilot-to-production conversion above 50%. Growth sourced from inside the financing ecosystem scores worse, not better — because it is the loop, not the market, doing the buying.

CoreWeave is the limiting case. 67% of its FY2025 revenue is a single counterparty — Microsoft, the unnamed "Customer A" in its 10-K — with the remainder committed by OpenAI, Meta, and Nvidia. Every named buyer is an investor in, or a lab funded by, the same circular structure. That is not independent adoption; it is recycled demand wearing a revenue label.

The honest reading is the one the NANDA anchor predicts: the "AI revenue" line grows fastest exactly where the demand is most recycled, and slowest where paid, arms-length conversion would actually prove it.

What would change our mind is specific and measurable: independent, retained, paying end-users converting pilots to production at scale, outside the financing loop. We will mark it the quarter the filings show it.

Read the full demand indicator → · Browse the 68-company board →