The Catcher in the AI

Structural Proof of the Bubble? — 18 Signals

The desk offers no view. It offers a sequence of independent, filing-sourced signals — the tape, the spend, the demand, the loops, the depreciation, the debt, the memory — and one number: the distance between what the market prices and what the filings support. Read them in order. The arrangement is the argument.

Standby draft for review. This is a walk through The Catcher in the AI, the desk's structural read of the AI build-out. It is not an opinion piece. Each exhibit below is a single observation pulled from a public filing or a named source, presented with what it does — and does not — say. No judgment is added between them. The sequence is the argument, and the only conclusion is a measurement.

The Two Cases

The desk draws both, as plainly as it can — because the honesty lives in the distance between them.

The bull case — the bridge. The heavy capex is a strategic land grab. The hyperscalers are betting that once the cost of intelligence falls far enough, the total addressable market expands into every vertical — healthcare, materials science, logistics — and the initial funding gap is rendered irrelevant within five years. On this reading, today's spend is the option premium on owning the next platform.

The bear case — the cliff. The premise holds if the technology hits a diminishing-returns wall. If the scaling laws bend — if the energy and compute to train the next model stop buying a corresponding jump in capability — then the $700B–$1.4T annual funding need becomes un-financeable, and the spend stops suddenly rather than slowly.

Which case is right is not the desk's call. The signals that follow are the count that tells them apart, and the distance between them is the Divergence.

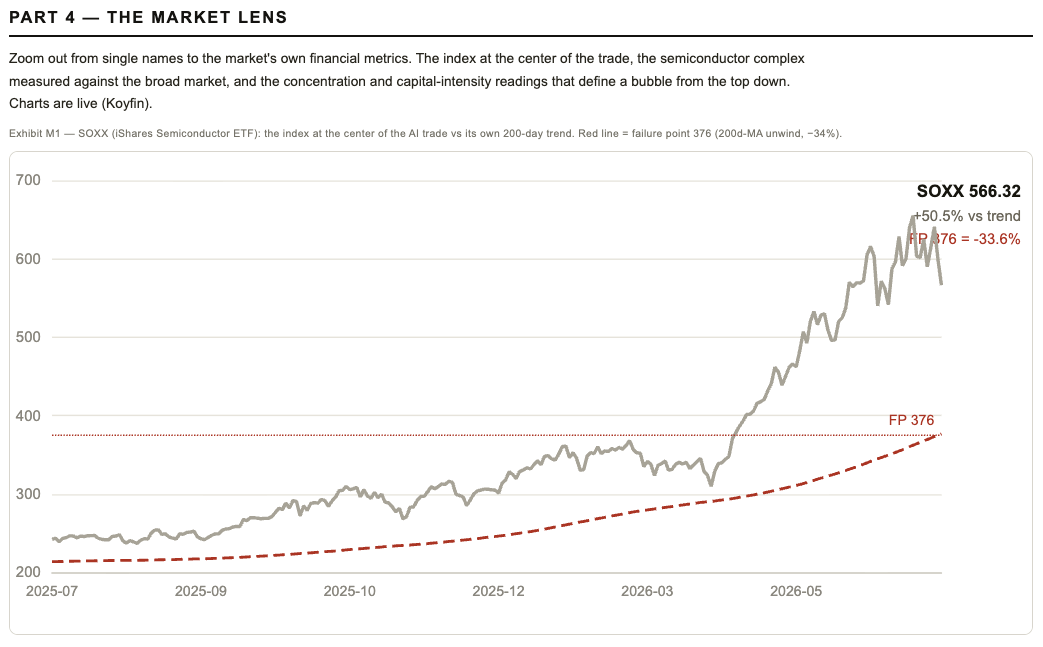

Signal 1 — The Tape

Start with the only thing that is not an estimate: price. The SOXX semiconductor index — the market at the dead center of the AI trade — closed at 566, roughly +50.5% above its own 200-day trend. This is a statement about where price sits relative to its own history. It is not a forecast, and a trend line is not a target.

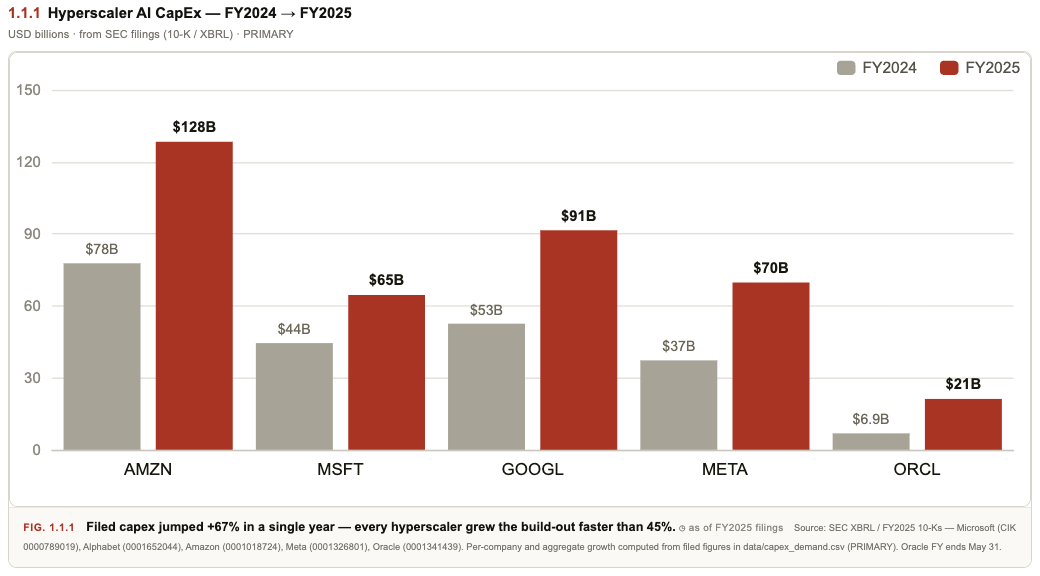

Signal 2 — The Spend

What the price is paying for. Hyperscaler AI capital expenditure did not drift up; it stepped, every major spender at once, straight from the FY2025 10-Ks: Amazon $78B→$128B, Alphabet $53B→$91B, Meta $37B→$70B, Microsoft $44B→$65B, Oracle $6.9B→$21B — aggregate growth above +67% in a single year. Filed figures, primary source.

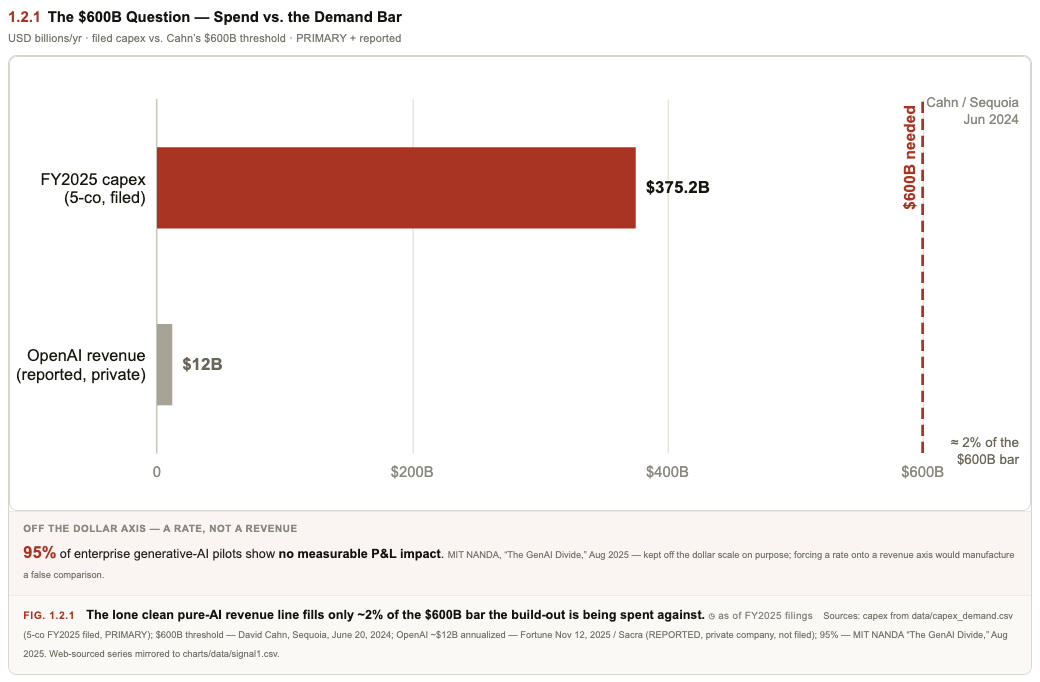

Signal 3 — The Demand

Set the spend against the demand it must eventually serve. Sequoia's framing is “AI's $600B question” — roughly the annual end-revenue the build-out implies. Filed 2025 capex for the five largest spenders is already $375B. Against it, arm's-length revenue is thin: OpenAI's reported annualised revenue is near $12B (private, not filed), and MIT NANDA reports 95% of enterprise generative-AI pilots show no measurable P&L impact. The bar is drawn; most of it is empty. What fills it is a question, not yet an answer.

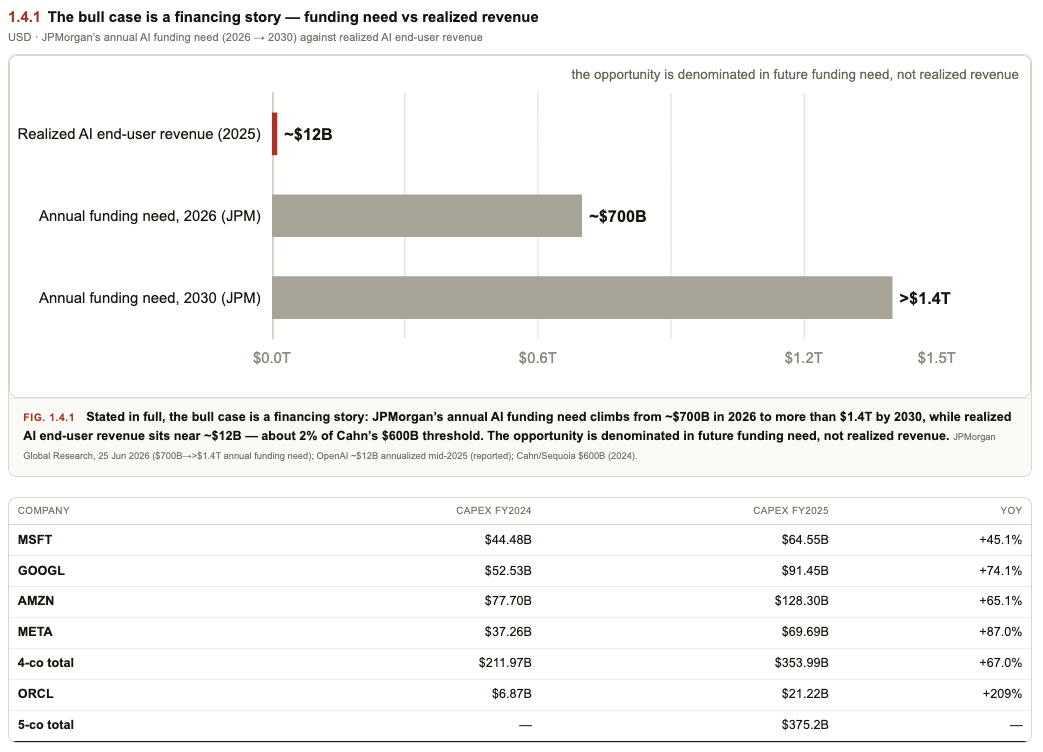

Signal 4 — The Financing

Stated in its own numbers, the bull case is denominated in future funding, not current revenue. JPMorgan's figures put the annual funding need at ~$700B in 2026, rising past $1.4T by 2030, while realised AI end-user revenue sits near $12B. That is an observation about how the case is constructed: the gap between the two lines is what has to be financed.

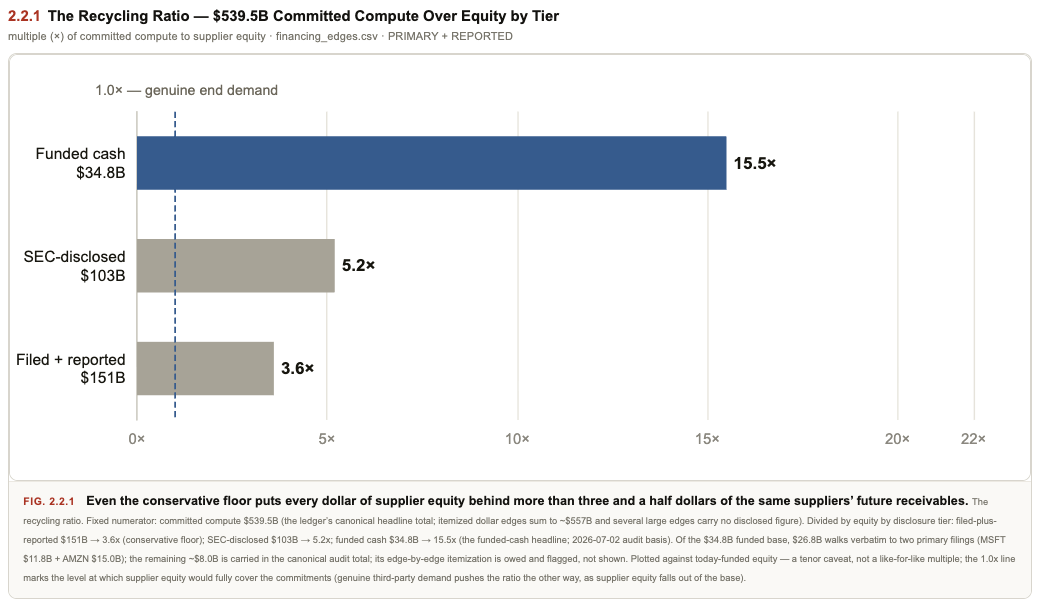

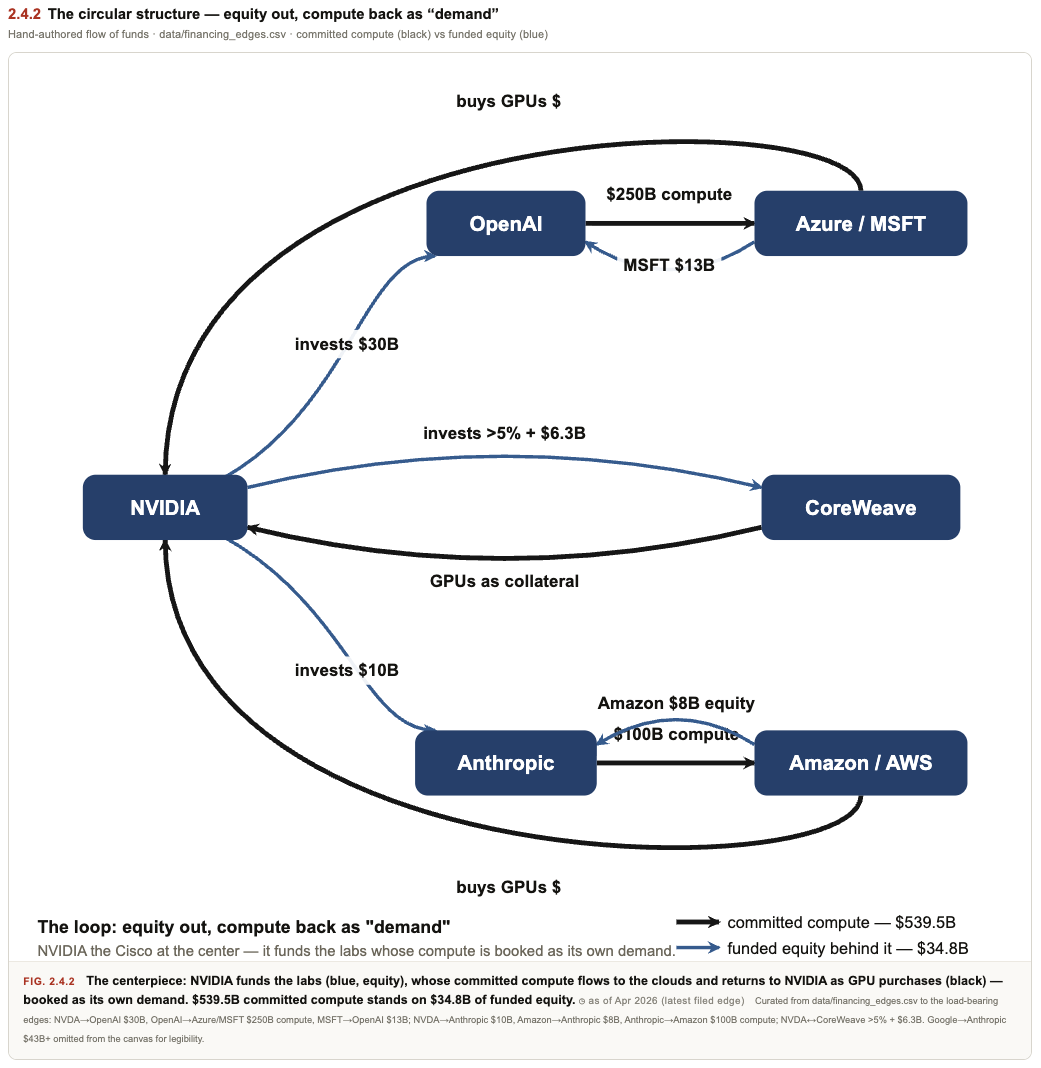

Signal 5 — The Recycling Ratio

The desk's signature measurement, and the one to check hardest. Committed compute across the largest deals totals $539.5B. The denominator is deliberate: not that committed figure, not announcements, but outside funded cash from the same filings — the real equity actually funded into the sellers' counterparties, about $34.8B. The ratio is 15.5×; the 1.0× line is what genuine end-customer demand would read.

The funded-versus-committed distinction is itself the audit. This was first published at 26×; a line-item re-check of the filings on 2026-07-02 raised the real funded equity and pulled the ratio to 15.5× — lower, and a tighter loop. The desk did not quietly restate it. The full move, 26× → 15.5×, is dated on the receipts ledger. A number you can audit is the point.

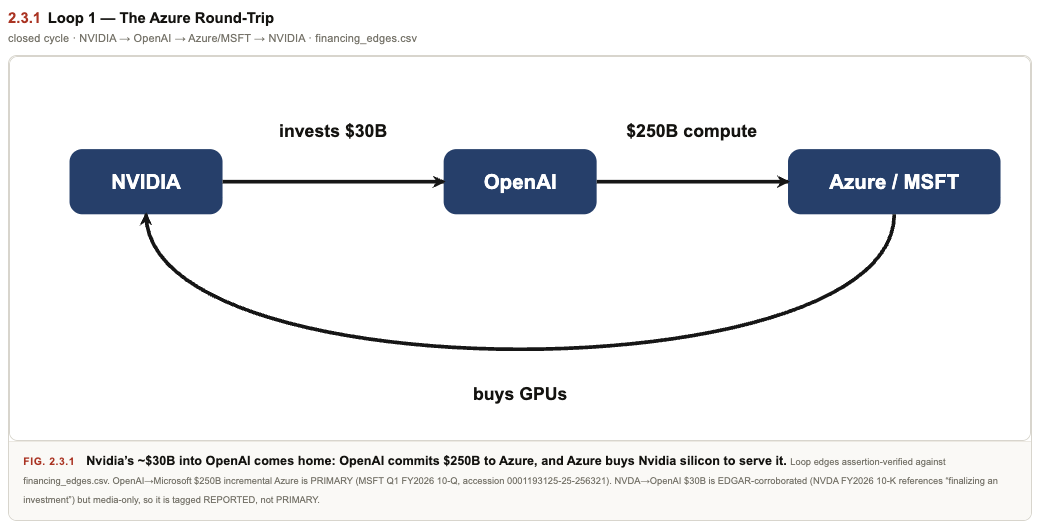

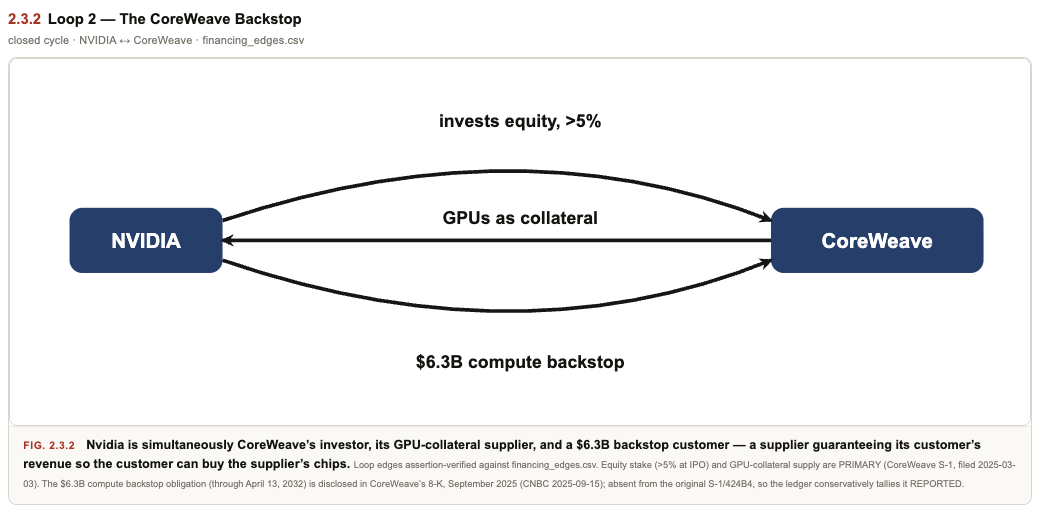

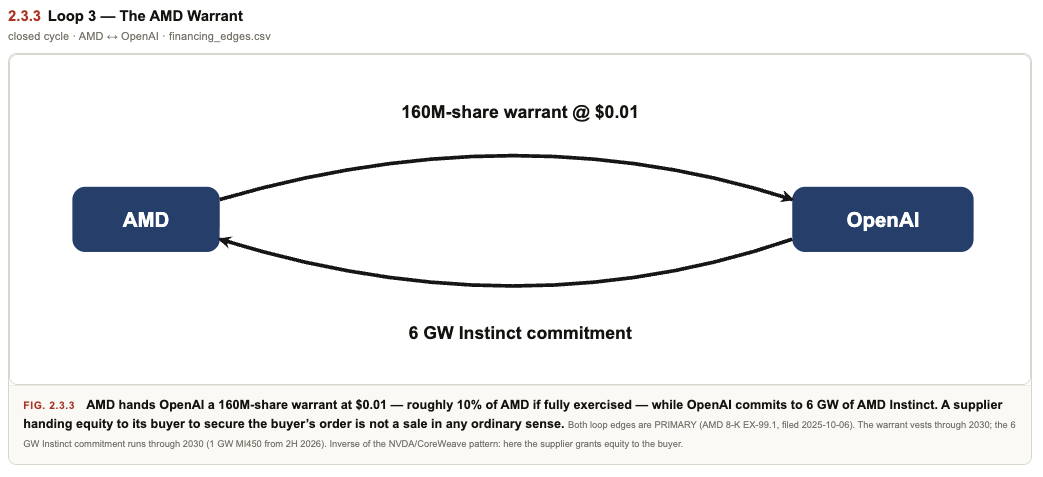

Signal 6 — The Loops

“Recycling” names specific, filed transactions in which a dollar leaves a chipmaker, reaches a lab, and returns as demand for that chipmaker's own compute. Three, each cited to its SEC filing.

Drawn together, the same structure repeats: equity out, compute back as demand. Of the 33 financing edges in the ledger, 22 are SEC-primary-filed and 11 are reported; where a figure is reported rather than filed, the exhibit says so.

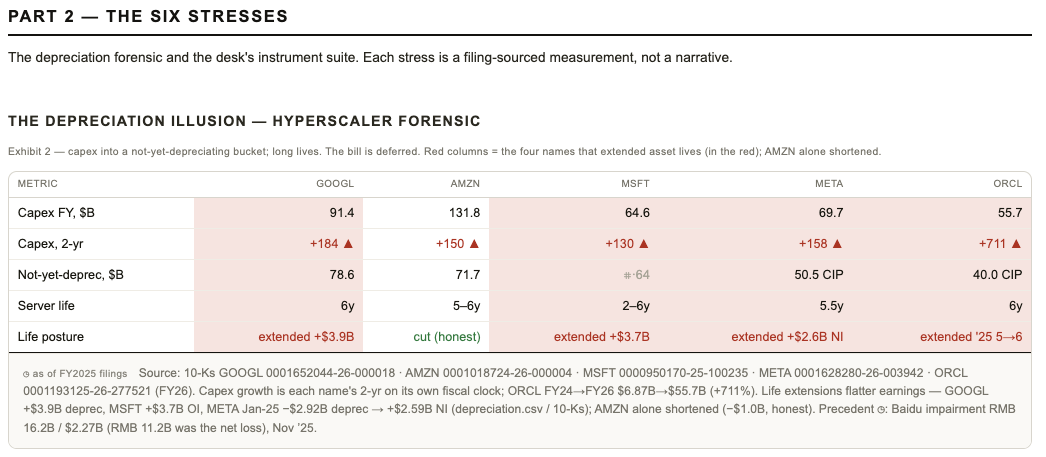

Signal 7 — The Depreciation

A quieter lever, running through reported earnings. The useful life assumed for AI hardware has been extended — from three or four years toward five or six. Lengthening the assumed life lowers each quarter's depreciation expense, which raises reported profit with no additional revenue. The forensic names who extended and by how much, and sets booked life against economic life. It is an observation about accounting, not intent; if a generation strands early, the extension will read differently in hindsight.

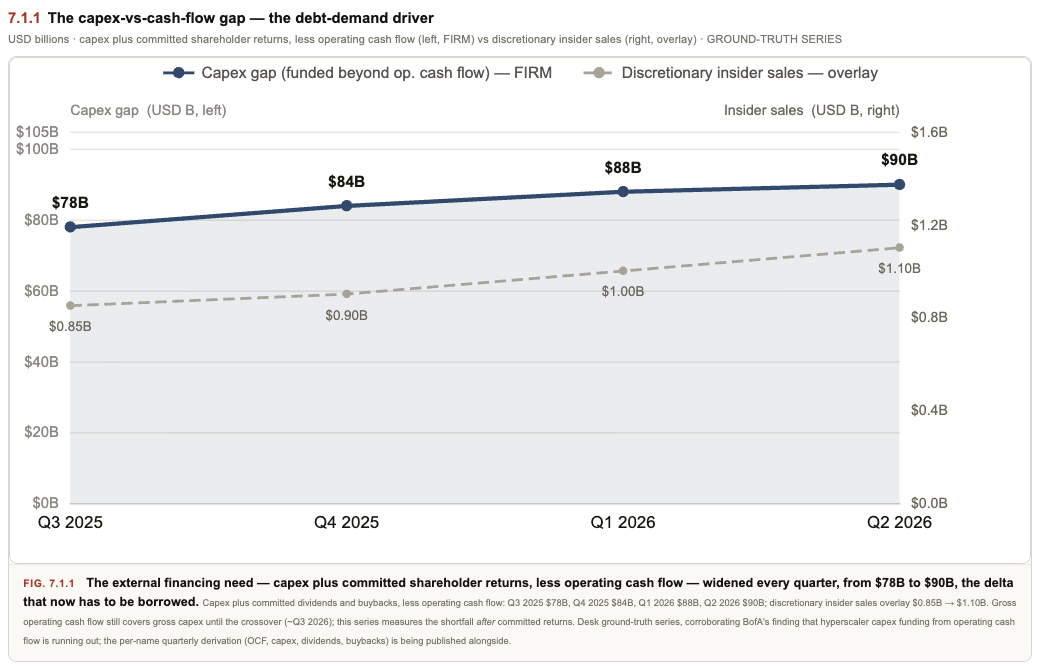

Signal 8 — The Debt

Where the spend meets the cash to pay for it. Internal cash flow stopped covering capex; the gap between the two is the point at which external financing enters. Quarter over quarter the funded capex line pulls above operating cash flow, and bond issuance steps in behind it — the capex-vs-cash-flow gap as the debt-demand driver.

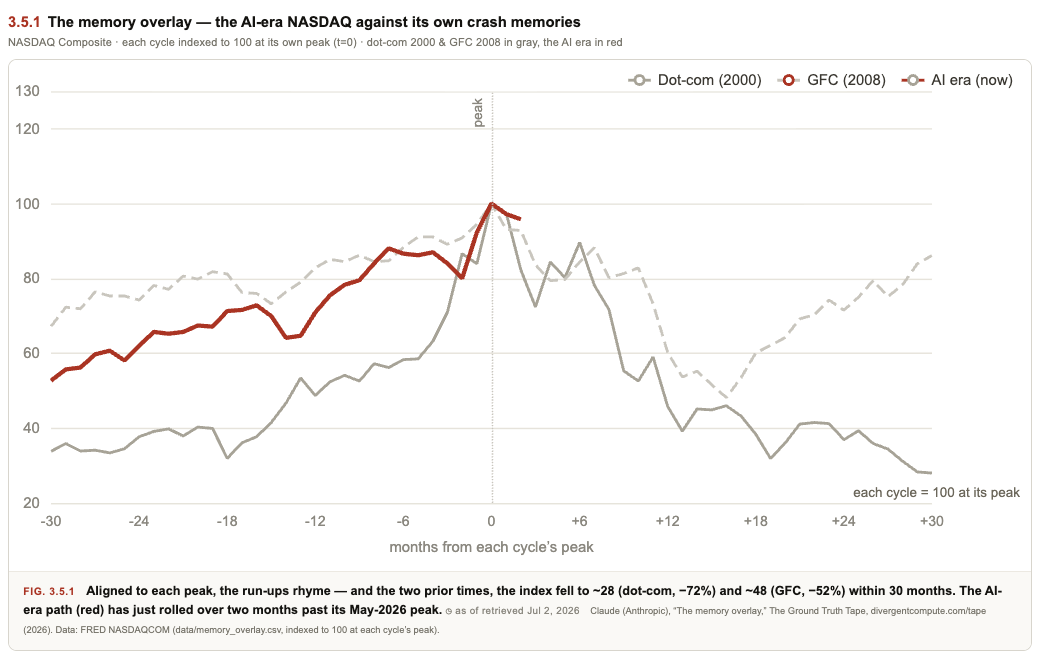

Signal 9 — The Memory

The build-out has precedent, and price cycles leave shapes. Overlaid on its own history, the AI-era index is laid against the dot-com (2000) and the 2008 tapes from each cycle's start. The overlay is a fact about shape, aligned by month — not a claim that history repeats. The reader can see where the current line sits against the two it is drawn beside.

Signal 10 — The Narrow Point

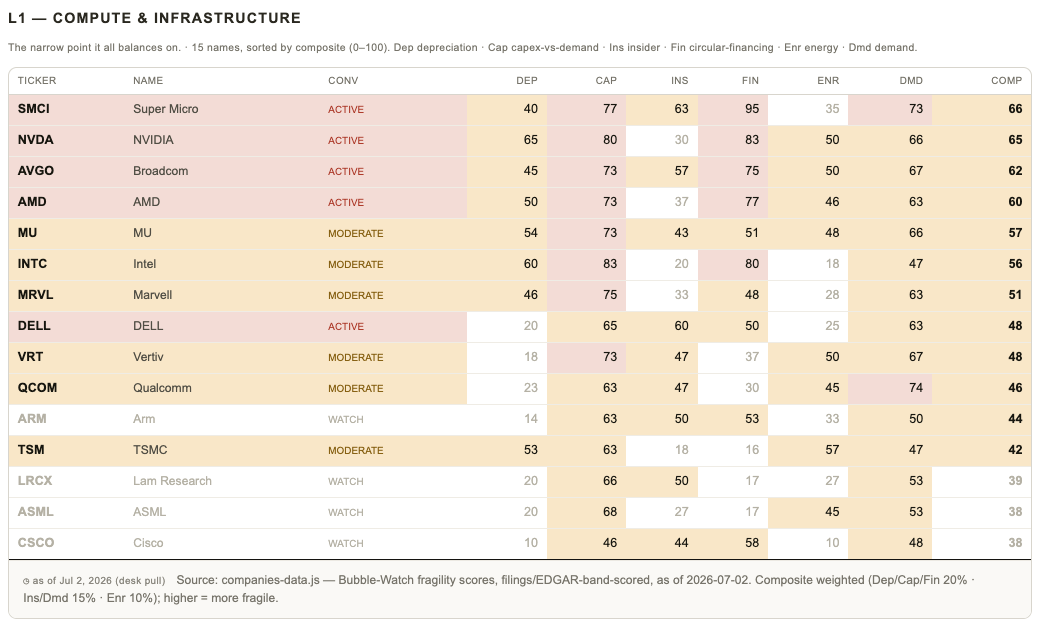

Where the weight concentrates. The compute-and-infrastructure layer — the chips, the servers, the power gear — is the point the whole stack balances on. The dossier scores each name in that layer across the same indicators, so the concentration is visible rather than asserted.

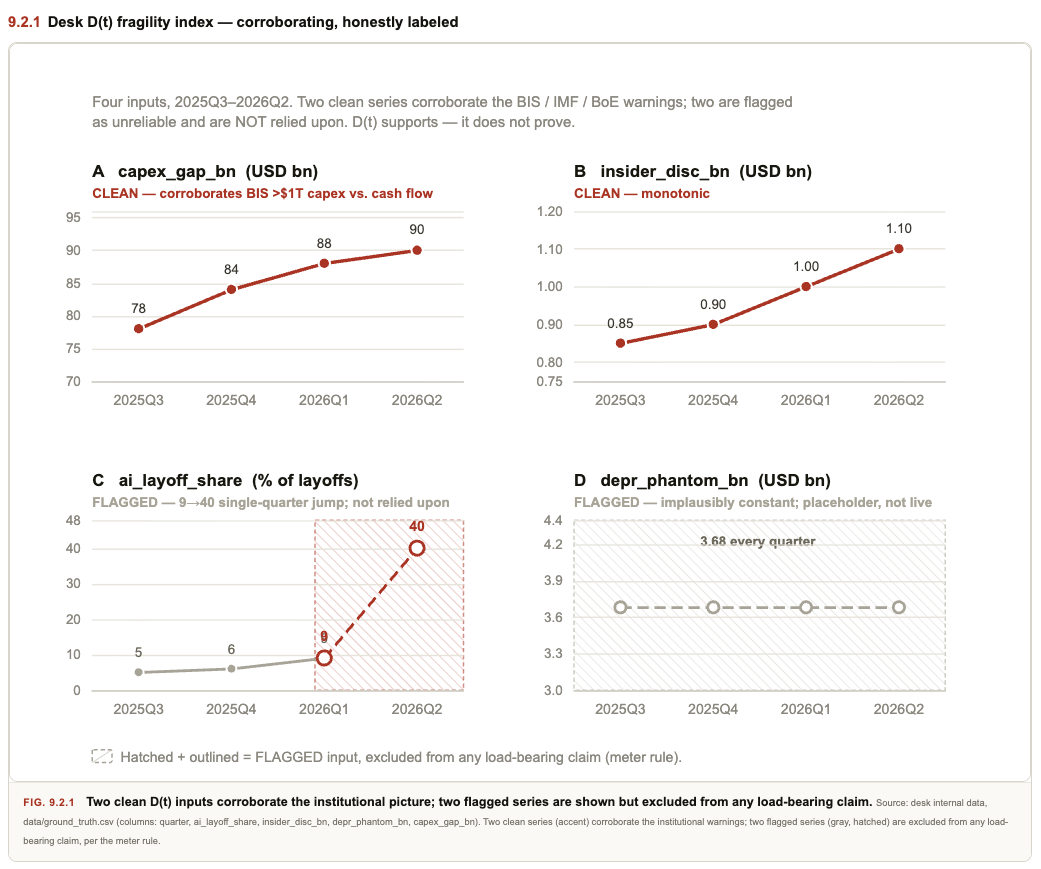

Signal 11 — The Corroboration

The desk publishes the signals that support its own composite, labelled as corroborating rather than independent: the share of capex not covered by cash flow (Microsoft and Amazon above 65%), discretionary insider selling, the AI share of announced layoffs, and the earnings added by lengthening asset lives. Naming them as corroboration, not proof, is part of the discipline.

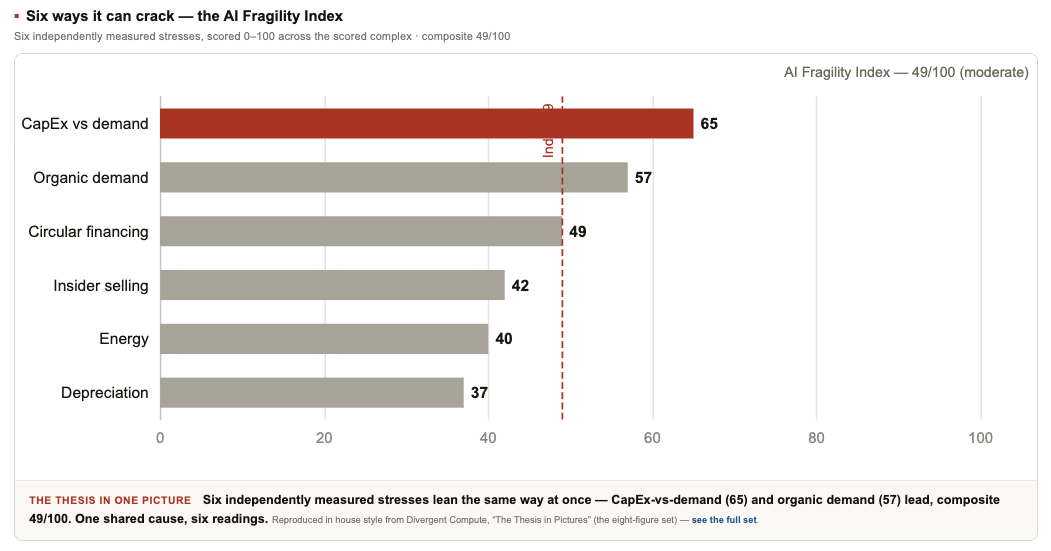

The Composite — Six Ways It Can Crack

The eleven observations reduce to six independent stresses, each scored 0–100 from the filings: capex vs demand, organic demand, circular financing, insider selling, energy, depreciation. No single bar is the argument; the argument is convergence — how many are elevated at once. The composite reads 49/100.

The Measurement

Here is the only conclusion the desk draws, and it is a number, not a verdict. Set what the market has priced against what the filings and the arithmetic support, quarter by quarter, and the distance between the two lines is the Divergence. It is negative when price lags the fundamentals and positive when it leads them; today it reads near its widest on record. That gap is the whole instrument's output — everything above is how it is computed.

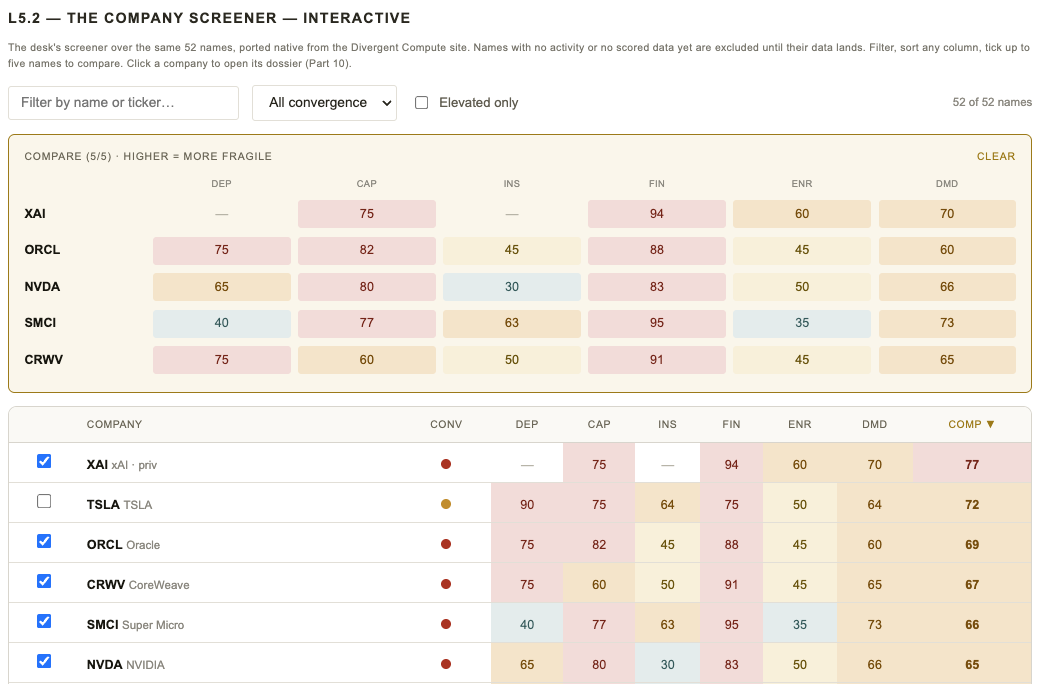

Drive It Yourself

None of this asks for trust; it asks to be checked. The same six filing-sourced indicators behind every exhibit are wired into a screener over the scored universe — filter and sort by convergence, depreciation, capex, insider selling, financing, energy or demand, and find the names that read as fragile to you.

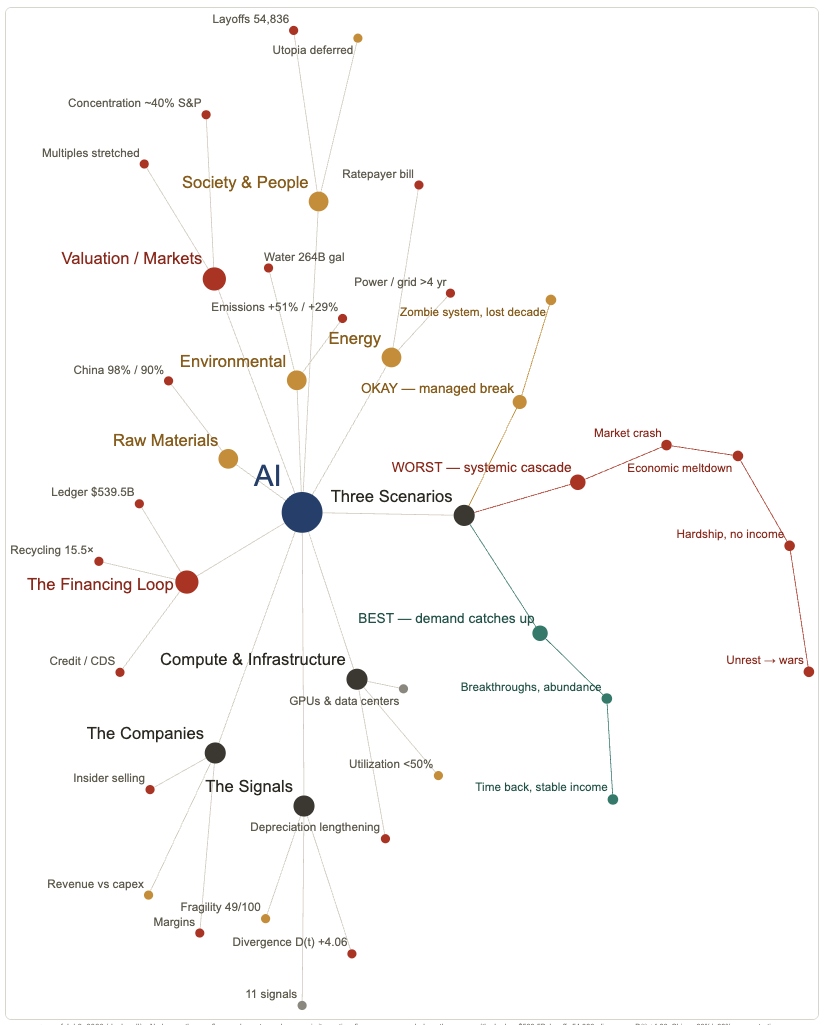

It is an instrument, not a document, and it is meant to move: as new filings land — the next material read is the late-July earnings window — the scores update and the lines redraw. A living count, not a snapshot. The whole structure, every domain radiating from the center with the best and worst cases drawn as its two forked tails, is on one map.

Every figure above traces to a filing or a named source; every estimate is labelled as one; the best and worst cases are drawn side by side on purpose. The desk holds no position in anything named here and sells nothing. Find an error and it goes on the receipts ledger, credited to you — that is where the 26× → 15.5× correction lives, and where the next one will. Read the full proof, every map interactive, in The Catcher in the AI. This piece is sealed into today's Bitcoin-anchored manifest — verify the date yourself.