AI — The Bigger Short or the Smaller Long?

Every position on the build-out reduces to one of two claims. We define both in numbers — and publish the tripwires that will move the fork when four AI balance sheets file in the same July week.

This is the desk’s framing piece for the July 28–30 filing window. When the numbers land, we will re-read it in public — same instruments, same tripwires, line by line.

The fork

Strip away the podcasts and the price targets, and every position on the AI build-out reduces to one of two claims.

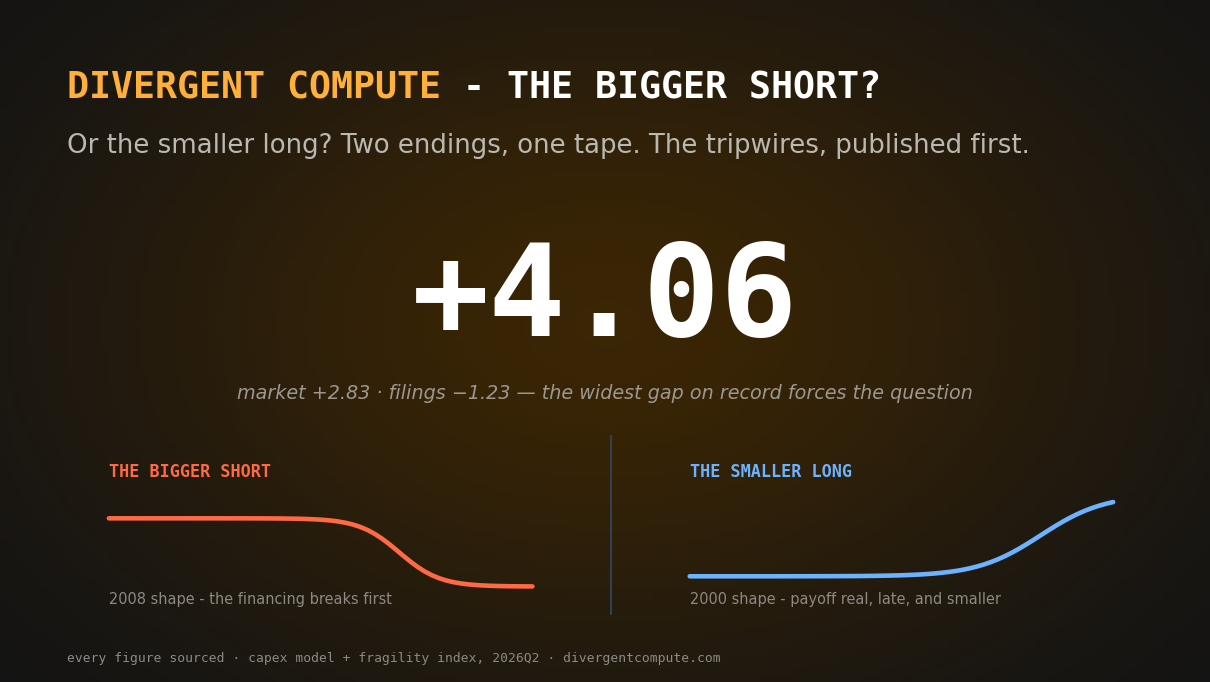

The Bigger Short: the financing structure gives way before the payoff arrives. The 2008 shape — not a technology failing, but a structure repricing faster than its collateral can bear.

The Smaller Long: the technology is real and the payoff comes — but later and smaller than the price assumes. The 2000 shape — right about the future, wrong about the invoice.

We run a research desk, not a book. Our job is not to pick a side; it is to state both claims in numbers and watch which one the filings feed. As of today the meter refuses to settle the question — and that refusal is the most honest reading on the tape.

What “bigger” would require

2008 was never about houses becoming worthless. It was about where the leverage sat: mortgage risk repackaged into instruments held by leveraged, mark-to-market institutions, so that when the collateral repriced, forced selling turned a housing slowdown into a systemic event. The short was bigger than the housing loss because the structure amplified it.

So the first question for the Bigger Short is structural: where is this cycle’s leverage? Mostly not in debt chains. The build-out is funded from the largest operating cash flows on earth. The frontier is where it gets interesting: ~$539B of committed compute rests on ~$35B of outside funded cash — 15.5× on the funded-cash basis, vendors financing customers whose commitments come back as the vendors’ own backlog. That ring is where a repricing would start.

And leverage is not entirely absent. CoreWeave’s $7.6B delayed-draw term loan is collateralized by the GPUs themselves (per its S-1) — depreciating collateral funding long-lived obligations, the closest structural rhyme to 2008 on our ledger. One more: the first server-life cut of this cycle is already on our depreciation indicator, citing AI obsolescence. Collateral schedules are how a ring reprices quietly, before it reprices loudly.

What the Bigger Short still lacks is a broad class of leveraged, forced-sale holders. What it already has is concentration and a market priced for perfection: the divergence sits at +4.06, the widest reading on record, and the Fragility Index reads 49/100 with capex-versus-demand at 65 — the hottest of the six indicators.

What “smaller” would require

2000 is the other rhyme: the internet thesis was right, and the people who priced it still lost. The fiber got laid, went dark, repriced — and the traffic eventually came, carried on capital someone else had written off. If that is the shape, the AI payoff is real, late, and cheapest for whoever buys the second lap.

Our meter gives this side real support. 19 of 31 industries show demonstrated AI ROI, with 9 more emerging; the adoption pace reads 69/100. Real, broad — and partial: nowhere near the scale of the spend. The lag between adoption and measured productivity is the desk’s second clock; Solow’s computers took a decade to show up in the statistics.

Cycle memory adds the timestamp. This build-out is in month 44 (from January 2023). The telecom cycle peaked at month 48. The overlay is a desk-labeled reading, not destiny — but it says the interesting quarter is soon, not someday.

What the tape says now

The divergence itself does not settle the fork. Market signal +2.83, ground truth −1.23, gap +4.06: what that says is that the market has already answered — long, and large. Both of our claims are therefore trading against the same price. The Bigger Short needs the filings to crack. The Smaller Long merely needs them to keep disappointing quietly while adoption grinds forward.

The tripwires

July 28–30, four of the largest AI balance sheets file within one week. The watch list is published in advance. Here is what would actually move the fork — stated now, so nobody has to take our word for it later.

Toward the Bigger Short: the recycling ratio widening on arm’s-length money rather than narrowing; a second server-life cut citing AI obsolescence — collateral repricing inside the ring; the financing and insider indicators converging upward to join capex-versus-demand above 60. Convergence, not any single reading, is the warning.

Toward the Smaller Long: AI-attributed revenue disclosures growing into the spend while capex growth decelerates without a price collapse; the divergence closing from below — filings improving toward the price; the demand indicator improving while the ring’s share of incremental commitments falls.

And the null: the filings may show neither. Then the fork stays open and we say exactly that on the receipts ledger. We have paid for that honesty before — the 15.5× headline is itself a public revision from 26×. We will pay it again.

The follow-up is already scheduled

The Bigger Short or the Smaller Long is not a question we can answer today — it is the question the next four quarters were built to answer. What we can do today is publish the instruments, the readings, and the exact conditions under which we would say we were wrong. When the window closes, we will write the follow-up against this page, line by line. The scoreboard is public. Bring your own position; we bring the meter.