Jevons or DWDM?

Every cut makes tokens cheaper — the bulls say cheaper tokens grow demand. The fiber cycle ran that exact experiment and collapsed anyway. One measurable variable decides.

This week SemiAnalysis published the sharpest version of the AI build-out’s best defense. Inference, they observed, keeps getting carved up — split by phase, by layer, and now by time itself — and every cut recovers wasted utilization. Recovered utilization lowers the cost per token. And then the conclusion: “We think cheaper tokens don’t shrink demand, they grow it.”

Every mechanical claim in that argument is correct, and we will not spend a sentence disputing the engineering. The last sentence, though, is not engineering. It is a belief about demand elasticity — the belief on which roughly $540 billion of committed compute rests. It deserves what beliefs that size deserve: a measurement.

The efficiency is real

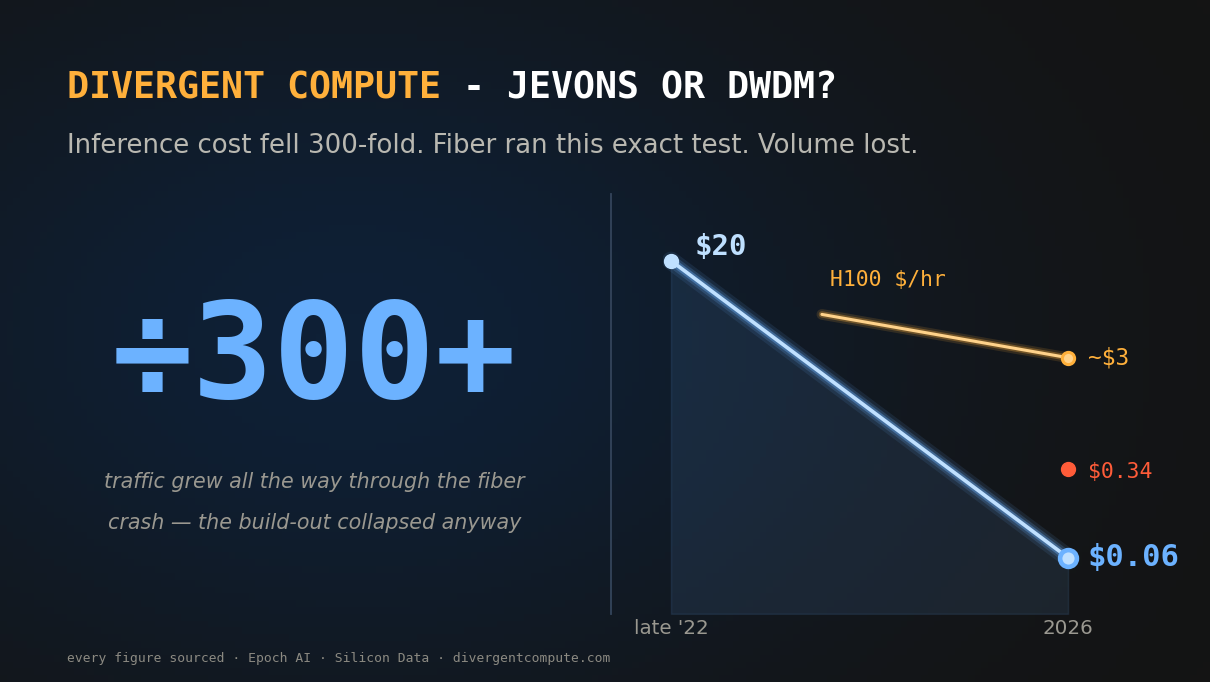

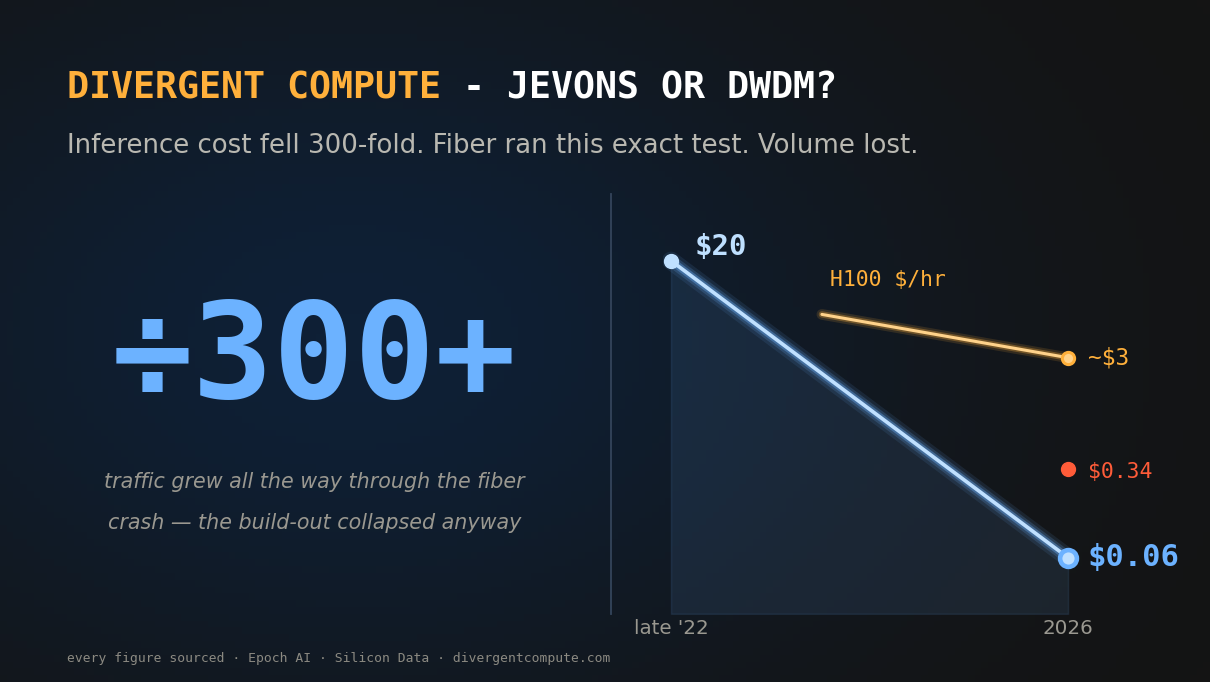

Grant the facts in full. Equivalent-capability inference prices have collapsed at a median of roughly 50x per year across benchmarked tasks — performance that cost more than $20 per million tokens in late 2022 sells for around six cents in 2026. H100 rentals that cleared above $7 per GPU-hour in early 2024 now trade near a $3 median, with spot capacity dipping under fifty cents. And usage has exploded to a scale measured in quadrillions of tokens annually. Cheaper intelligence, more consumption. So far, Jevons is winning on volume.

But volume was never the question.

The last cycle ran this exact experiment

The fiber build-out of 1996 to 2001 had its own efficiency miracle: dense wavelength-division multiplexing. DWDM multiplied the capacity of already-laid fiber by ten to a hundred times — capacity per dollar rising by orders of magnitude, right as half a trillion dollars of debt-financed glass went into the ground.

Here is the part that matters: demand kept growing. Internet traffic rose all the way through the crash. Volume never stopped expanding — and the industry collapsed anyway, because capacity per dollar grew faster than dollars arrived. Bits exploded; revenue per strand went to zero; more than $2 trillion of equity value followed. Growing demand did not save an industry whose efficiency outran its income.

That is the precise flaw in resting a build-out on Jevons: the paradox speaks to usage, but debt and capex are serviced in dollars.

The test that decides it

So the deciding variable is not whether tokens get cheaper (they will), nor whether usage grows (it will). It is dollar-elasticity: when the price of intelligence falls tenfold, does revenue grow by more than tenfold — or less?

The early evidence cuts both ways, which is exactly why it needs a meter and not a slogan. Revenue at the leading labs has grown severalfold through the price collapse — real, dollar-denominated growth; Jevons has a case. But an honest reading of 2026 adds a wrinkle: effective token pricing has fallen only about 6 percent year-to-date — the easy deflation is decelerating — while the committed capacity from the 2024–2025 ordering cycle is still arriving, and one hyperscaler has already begun renting out its excess. Efficiency gains stack on top of a fleet that is still growing. Supply per dollar is compounding from two directions at once.

What we will measure

We are adding an efficiency series to the desk’s public instruments: frontier token prices over time, GPU rental rates, and — each quarter, from the filings — reported AI revenue against our estimate of deployed capacity-per-dollar. The condition for the bull case is crisp: revenue must outrun capacity-per-dollar. The condition for the fiber outcome is equally crisp: it must not.

Falsifiers, stated in advance, both directions. If AI revenue keeps compounding through the price collapse faster than efficiency and fleet growth expand supply, Jevons wins, the build-out pays, and we will publish that trajectory as prominently as any warning. If revenue growth decelerates while capacity-per-dollar accelerates — the fiber signature — the tape will show it quarters before the narrative admits it.

The 2000 cycle taught the industry a word for capacity that demand was supposed to fill: dark fiber. Whether the AI cycle earns its own word is not a matter of opinion. It is a measurement — and it is now on the tape.

The live measurement: Jevons or DWDM? · the fiber overlay: AI vs Dotcom · the tape: The Ground Truth Tape